According to MAR's Commission Delegated Regulation (EU) 2016/522 of 17/Dec/2015, wash trading consists in entering into arrangements for the sale or purchase of a financial instrument where:

- There is no change in beneficial interests or market risk (A); or

- Beneficial interest or market risk is transferred between parties who are acting in concert or collusion (B).

On its hand, the term matched orders is oftenly used to refer to the orders placed with the intent to generate wash trades (as the manipulator matches one order with the other).

Nonetheless, MAR's Commission Delegated Regulation (EU) 2016/522 of 17/Dec/2015 defines improper matched orders as the practice of pursuing transactions by entering buy and sell orders to trade at or nearly at the same time, with very similar quantity and similar price, by the same party or different but colluding parties.

I will refer to all of these transactions as wash trades, and will consider that they can be categorized in three types (these terms were coined by me, so do not expect to see them being used out there): pure wash trades, camouflaged wash trades and quasi wash trades. On its hand, I will use the term matched orders to described the orders that are placed with the intent to generate wash trades.

Those three types of transactions that I am calling wash trades are exactly the same in what regards manipulative intention, and are similar in style. In fact, the US SEC also seems to call all of such as wash trades, as it stated in a 2014 Administrative Proceeding: "wash trading is the purchase and sale of a security, either simultaneously or within a short period of time, that involves no change in the beneficial ownership of the security, as a means of creating artificial market activity".

Those three types of transactions that I am calling wash trades are exactly the same in what regards manipulative intention, and are similar in style. In fact, the US SEC also seems to call all of such as wash trades, as it stated in a 2014 Administrative Proceeding: "wash trading is the purchase and sale of a security, either simultaneously or within a short period of time, that involves no change in the beneficial ownership of the security, as a means of creating artificial market activity".

Pure wash trades: Here, I am referring to the most iconic form of wash trading, which is when a person (or colluding persons) is simultaneously the buyer and the seller in the same transaction.

Camouflaged wash trades: Here, I am referring to the situations in which a person (or colluding persons) buys and sells a financial instrument in different transactions in the same quantity and at the same price (which can be achieved through the use of limit orders). I refer to this type of trading practice as camouflaged wash trading due to the fact that, although the manipulator (or colluding manipulators) is not in both sides of the transactions, there is still no change in beneficial interests and the market risk is very limited. Indeed, there is some risk, derived from the fact that, due to abrupt changes in market conditions, the manipulator may fail to execute the second (reversal) transaction. In principle, as wider is the time span between the buying and the selling of the securities, the larger is the market risk.

Quasi wash trades: Here, I am referring to the situations in which a person buys and sells a financial instrument in different transactions in similar quantities and/or at similar prices (possibly through the use of market orders). I refer to this type of trading practice as quasi wash trading due to the fact that, although the manipulator (or colluding manipulators) is not in both sides of the transactions, there is still no change in beneficial interests and the market risk is contained. Indeed, there is risk, derived from the fact that the first and second (reversal) transactions are made at different prices. In principle, as wider is the time span between the buying and the selling of the securities, the larger is the market risk.

Note that the two latter practices (camouflaged wash trading and quasi wash trading) are not possible in a market with zero (or almost zero) liquidity, as in such the manipulator does need to be in both sides of the trade. But may be feasible in a market where liquidity is low, as long it is high enough to execute trades whenever necessary.

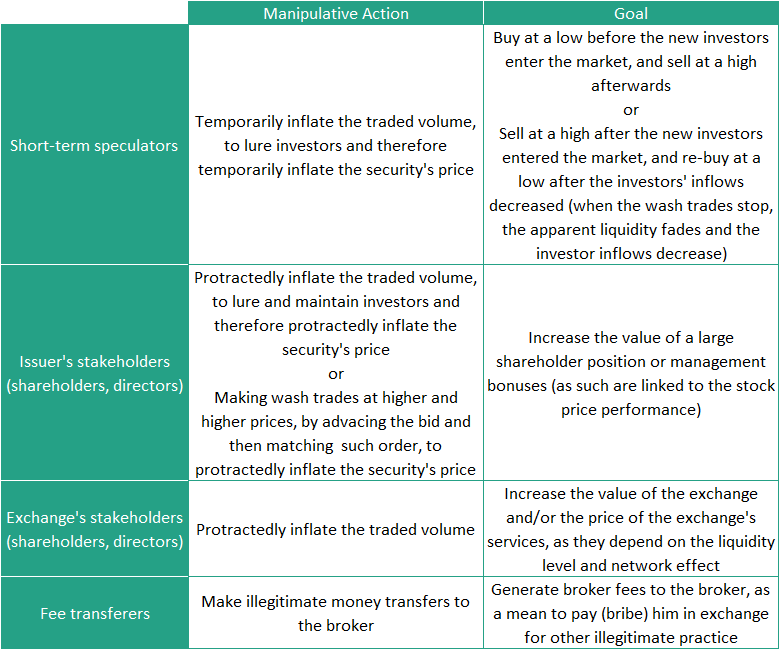

Wash trading may be done for different purposes, such as the ones described in the table below.

Note that the two latter practices (camouflaged wash trading and quasi wash trading) are not possible in a market with zero (or almost zero) liquidity, as in such the manipulator does need to be in both sides of the trade. But may be feasible in a market where liquidity is low, as long it is high enough to execute trades whenever necessary.

Wash trading may be done for different purposes, such as the ones described in the table below.

Comments

Post a Comment